How to Plan and Invest for Your Child’s Foreign Education Goal

Have you ever imagined your child walking through the gates of a top international university, studying in a beautiful new country, learning new skills, and making their dreams come true? It’s a proud moment every parent dreams of. But while the goal is exciting, the cost of foreign education can be quite overwhelming.

If your child plans to study abroad in the next 5 to 7 years, the best thing you can do today is start planning your finances. The earlier you start, the easier it becomes to build a strong education fund without stress. In this article, we’ll break down a simple, step-by-step investment plan to help you prepare smoothly and smartly, no financial background required.

Start with the end goal in mind

Before you begin investing, you need to understand what you’re working toward. Think about where your child wants to study, the course they’re interested in, and how long it will last. These details will help you estimate the full cost, not just tuition, but also accommodation, travel, and daily expenses.

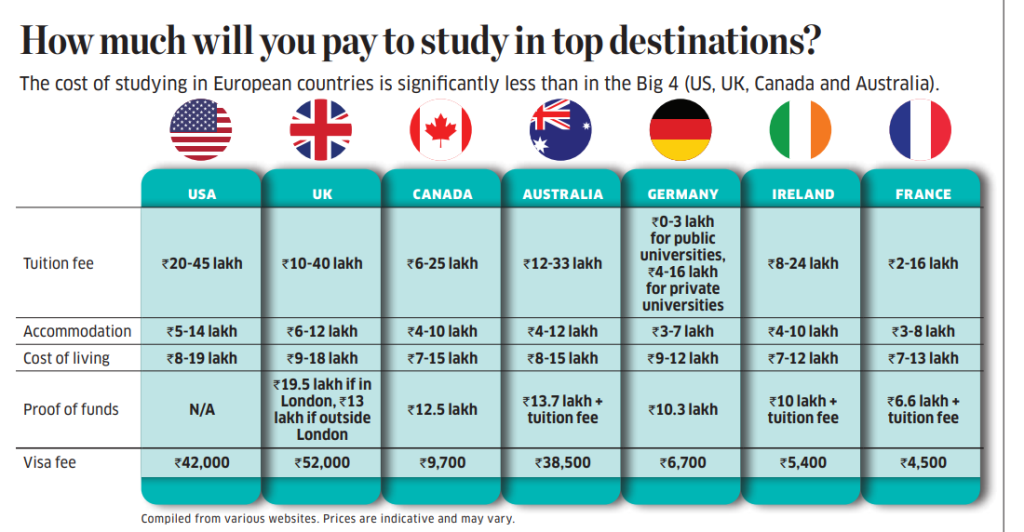

But costs don’t stay the same over the years. Due to inflation, education fees increase by approximately 8-10% each year. And since you’ll be paying in a foreign currency, you’ll also need to watch exchange rates. Once you know how much the future cost might be, convert that amount to Indian Rupees (INR) and make it your target.

Here’s a chart to help you understand how much you have to pay to study in these top destinations:

Now that you have a clear goal, the next step is to understand how much time you have to reach it and how much risk you can take along the way.

Understand the time horizon and risk appetite

Your investment choices depend a lot on your time frame. If you have 5 years or more, you can afford to invest in equity-focused options, which grow well over time but can be a bit bumpy in the short term. If you have only 3 – 4 years, it’s safer to go with more balanced or conservative options that offer steady, if smaller, returns.

Also, take a look at what you’ve already saved and compare it to the goal amount you just calculated. This will show you the gap you need to cover and help you decide how aggressively you need to invest.

With this in mind, let’s look at the best ways to invest your money based on your timeline and comfort with risk.

Choose the right investment instruments

Now that you know your goal, timeline, and risk level, it’s time to pick the right tools. Not all savings methods grow your money the same way.

- Mutual funds through SIPs (Systematic Investment Plans) are a great choice. You invest a fixed amount monthly, and it grows steadily over time.

- International or index unds give you global exposure and can help protect against changes in currency value.

- Debt funds or fixed income options are safer and good for use in the final years before your child leaves.

Many people use fixed deposits or savings accounts, but these may not grow fast enough to beat inflation. That’s why choosing the right mix of investment options is key.

Now, let’s talk about how you can grow your investment power over time without feeling the pinch.

Step-up strategy: Increase SIPs over time

As your income increases over the years, your savings should grow too. That’s where a step-up SIP strategy comes in. By increasing your monthly investments every year, even by a small amount, you stay on track to meet your goal without needing to invest a huge sum all at once.

For instance, starting with ₹20,000 per month for 7 years, and increasing your SIP by 10% annually, with an expected return of 12%, can help you build a corpus of over ₹34 lakhs. In contrast, if you had continued with a flat ₹20,000 SIP without any increase, the corpus would be just around ₹26 lakhs. That’s a difference of more than ₹8 lakhs that can be achieved simply by increasing your contribution gradually over time.

This method makes investing feel manageable and flexible. It’s also smart to review your plan once a year and make changes based on your progress or life changes.

And as you move closer to the goal, your strategy should shift from growth to safety. Let’s see how to make that transition smooth and secure.

Transition from growth to protection closer to the goal

About 12 to 18 months before your child needs the funds, it’s wise to start moving your investments from equity (which can be volatile) to debt (which is more stable). This helps protect the savings you’ve built from sudden market drops.

To stay organised, consider creating a separate education fund so it doesn’t get mixed with money meant for other goals, like a home or retirement. Protecting your investment in the final stage is just as important as growing it in the beginning.

But when investing for foreign education, there’s one more thing to keep in mind: currency risk. Let’s understand how this can affect your savings.

Track currency risk (Optional but useful)

Because your expenses will be in a foreign currency (like USD, Euro, or GBP), the exchange rate plays a big role. If the Indian Rupee weakens over the years, you may need more INR than you originally planned.

One way to reduce this risk is to invest in international mutual funds or ETFs that invest in international markets. This acts like a natural protection against currency changes. Also, it’s a good habit to review your total goal once a year and adjust for any major currency shifts.

Once you’ve planned your investments, the next thing you need to understand is how to legally send the money abroad when the time comes.

Understand the LRS (Liberalised Remittance Scheme)

The Liberalised Remittance Scheme (LRS) by the RBI allows every Indian resident to send up to USD 250,000 per financial year for education and other permitted purposes. That means each parent can send this amount individually, giving you a combined limit of USD 500,000 if both contribute.

This covers tuition fees, living costs, books, and more. But remember, this must be done through approved banks or financial institutions. Also, a Tax Collected at Source (TCS) of 5% – 20% may be applied based on the total amount and reason for the transfer.

Many parents also set up an offshore investment account through the remittances to earn a minimal interest rate but protect their capital from Indian rupee depreciation.

So, plan your remittances ahead of time and make sure you account for all paperwork and taxes involved.

Even with all this planning, it’s smart to prepare for the unexpected. Let’s look at how to do that.

Have a Contingency Fund

No matter how well you plan, life can be unpredictable. What if there’s a delay in fund transfers? Or a job loss? Or a health issue? That’s why it’s important to keep 6–12 months of expenses in a liquid fund, money that’s easy to access when needed.

This emergency fund should be completely separate from your education savings. Think of it as a safety net that gives you peace of mind while your main investments work toward your child’s dream.

Conclusion

Planning for your child’s foreign education is more than just saving money, it’s about building a thoughtful, flexible, and realistic strategy. When you start with a clear goal, choose the right investments, and understand things like currency risk and remittance rules, you reduce future stress and increase your child’s chances of success.

Keep reviewing your plan every year, stay consistent with your SIPs, and adjust as needed. Most importantly, start now. Because while the best time to begin was yesterday, the second-best time is today.

Your child’s dream deserves a strong foundation. You have the power to build it, one step at a time.

Prasad Iyer

[Certified Financial Planner – CFP CM]