Market Cap: Market capitalization shows the size of the company and its aggregate value.

Market Capitalization = (Total no of outstanding shares) * (Price of one share)

Outstanding Shares refers to all shares currently owned by stockholders, company officials, and investors in the public domain.

Take an example of Reliance Industries as of today,

Market Cap = (Total no of outstanding shares) * (Price of one share)

Reliance Market Cap = 61,71,002 * 2345 = 144,710.11 Lacs = ~14.41 Billions INR

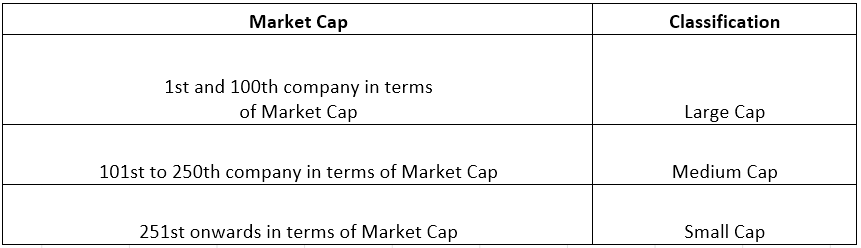

Large, Mid and Small Cap

There is no hard and fast rule for categorization of the companies based on the market capitalization. If you refer to different financial websites, the range of market cap will vary for different capitalization. In general here is the commonly accepted classification of companies based on the market capitalization in Indian stock market. (as per SEBI guidelines)

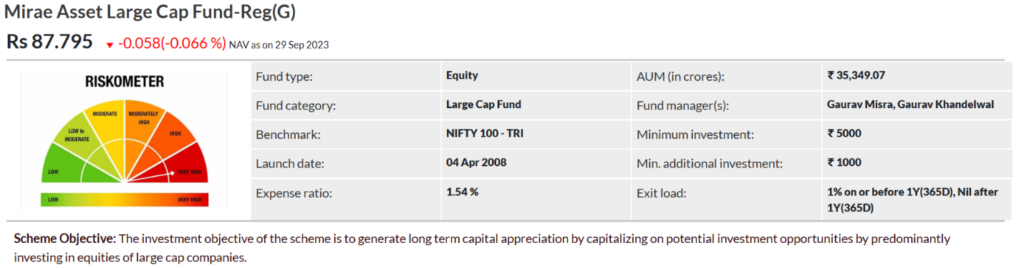

Mirae Asset Large Cap Fund – Regular Plan

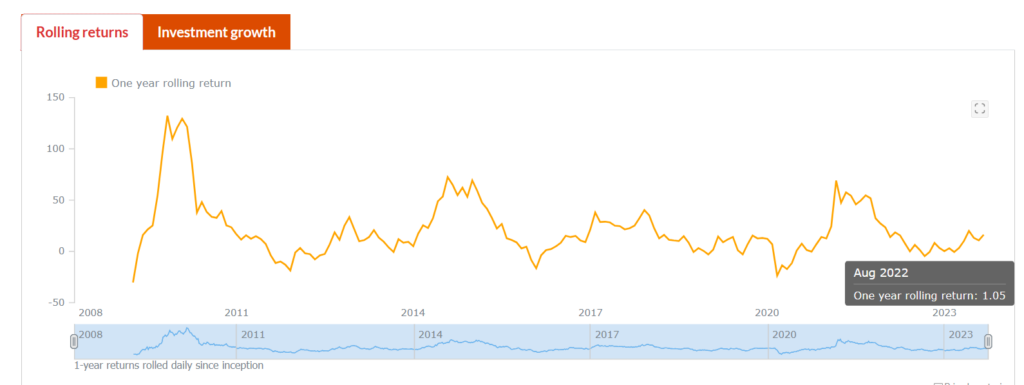

As you can see for Mirae Asset Large Cap the NAV as of 29 Sep 2023 is 87.795 with an expense ratio of 1.54%. Its rolling return displayed of 1 year period is 1.05% and this can be computed for various cycles and time periods. The AUM of the mutual fund which is total asset under management is 35,349 INR Crores as of the date. Its investment returns compared to its benchmark is displayed over multiple years as below

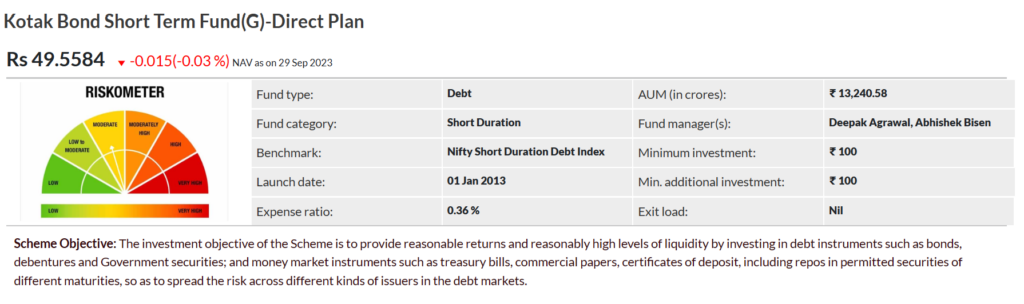

Kotak Short Term Bond Fund – Direct Plan

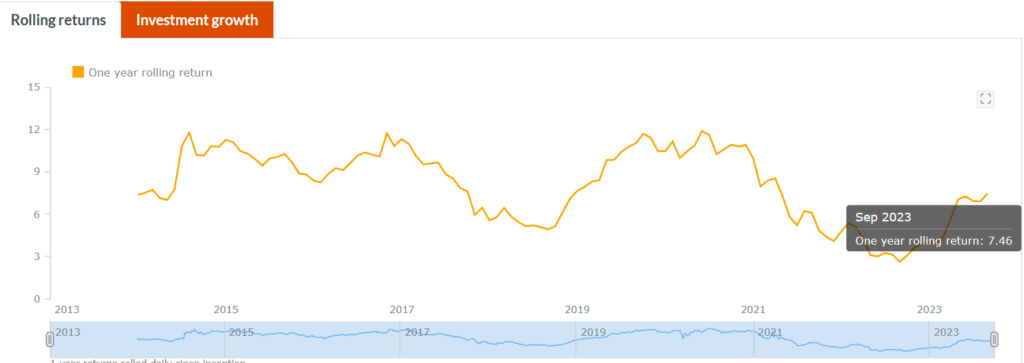

Kotak Bond is a Debt fund with rolling returns of 7.46% as of Sept 2023 with a AUM of 13, 240 Crores, expense ratio of 0.36% and with a moderate risk profile as per Riskometer. It’s a capital preserving fund which provides returns adjusted over inflation over longer period of time as can be seen in the table below

If you are a beginner, the above information should suffice to understand the basic nomenclatures used related to mutual fund investments and make you a little more confident discussing or considering this asset class to achieve your financial goals. Any more feedback please do reach out to us directly at info@kyronfinserv.com or leave a comment at the bottom of this blog.

Disclaimer: All the funds mentioned in examples are randomly chosen and not any recommendations. Please engage your financial advisor or mutual funds distributor before making any investments.

Image and Data Source: Various social media sites including Money-Control, AMFI etc.